After a year strong absolute and relative returns, can Mexican stocks keep delivering? Federico Galassi, Mexico Portfolio Manager, shares his macro and policy outlooks, along with areas where he is finding value.

Luis Arcentales: Fede, Mexico outperformed EM stocks by a wide margin since 2025. The good returns came despite the seemingly bearish mix of US protectionism and disappointing growth. What’s your take on why Mexican stocks did so well? And do you see any lessons for the rest of 2026?

Federico Galassi: Yes, Mexico had a good run rising over 70% since 2025. One caveat: peso strength accounted for roughly 75% of the 33p.p. outperformance versus the EM index.

As for why Mexico did well, the market was historically cheap in early 2025. That followed the big de-rating in the second half of 2024 after Mexican presidential elections and then the November US vote. If you look at the broader market behavior last year, valuations mattered: for some of the biggest winners like Colombia and Korea or laggards like India, starting valuations were an important factor driving returns1.

Another driver, I think, was Mexico getting a lift from the wider optimism about EM and global diversification. Anecdotally, I’ve seen a lot more interest from foreign investors, both global and dedicated, in the past year. Last, materials account for about 30% of the index, so rising commodity prices helped, too.

LA: What about the fears over rising US trade protectionism?

FG: Well, I’d say that the US protectionist bark turned out to be worse than the bite so far. I don’t want to minimize the risk to Mexico’s economy, which relies on the US for 83% of all export demand. But if you look at the numbers, exports keep rising and Mexico’s 16% market share in the US is an all-time high. Effective tariffs on Mexico are lower than other large trading partners’ thanks to the carveout for USMCA-compliant goods2.

Moreover, investors seemed to take comfort from the proactive response by President Sheinbaum to tariff threats by strengthening collaboration on security and by slapping tariffs mainly on China3. This pragmatic approach is understandable given Mexico’s limited leverage in any trade negotiation.

LA: But Mexico saw a string of downward GDP revisions so this positive export trend didn’t translate into stronger growth.

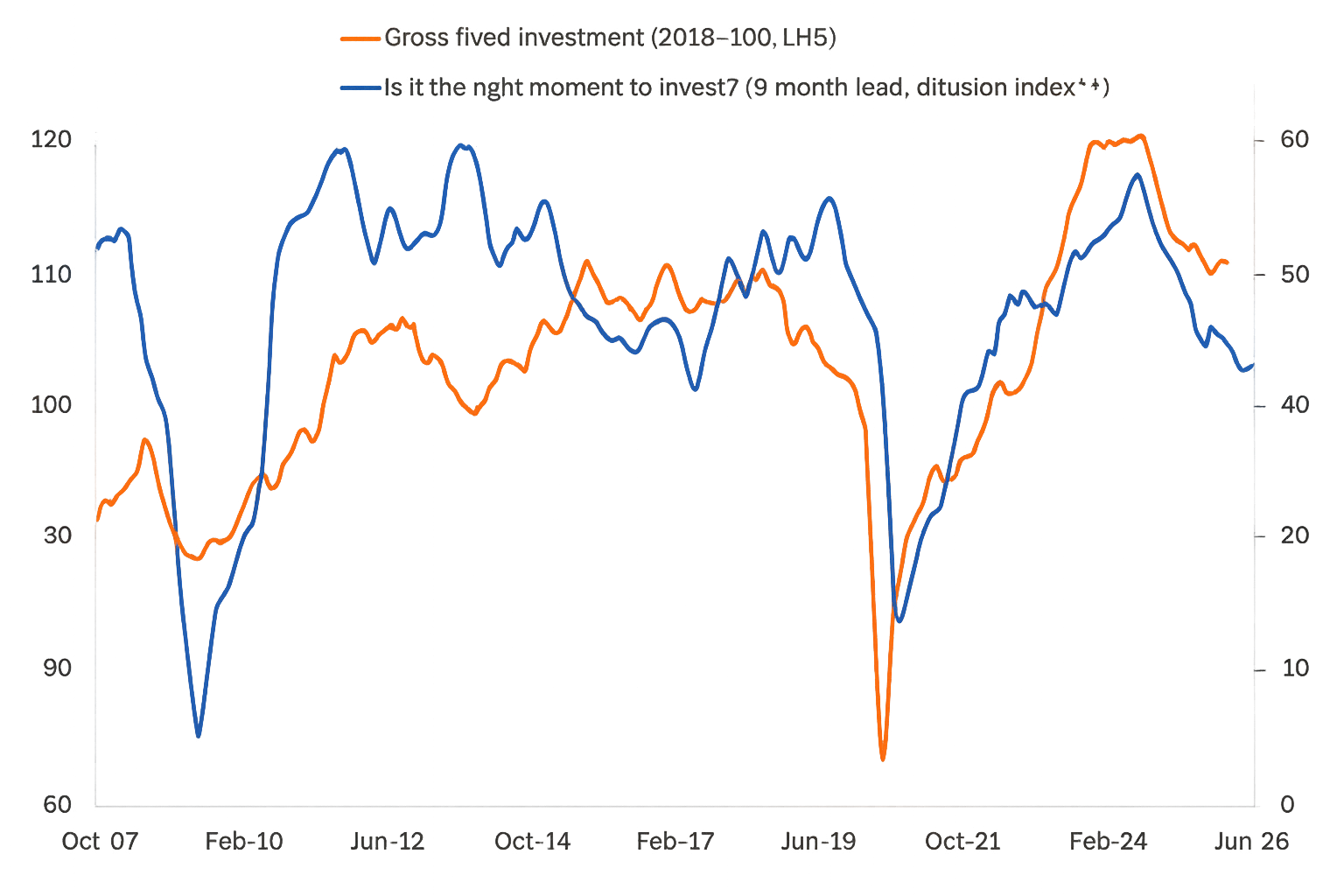

FG: Yes, that’s right. Export growth wasn’t the issue but the drag from weak investment associated to USMCA uncertainty. Remember the nearshoring narrative? Well, that began to fade once the future of regional integration and USMCA came into question, compounding lingering concerns over electricity supply (see Figure 1). The government recently launched a public-private investment plan, which may partly offset the ongoing capex slump4. Let’s see if policymakers manage to offer compelling terms and conditions to private players.

LA: You noted that President Sheinbaum has been instrumental in helping the country navigate the US’ shifting policy priorities in trade, immigration, crime. Do you think the recent electoral reform setback diminishes her ability to respond to future US demands, including ongoing USMCA negotiations?

FG: I don’t really think the defeat matters for governability going forward. It wasn’t about ideology but survival for the opposition, since the changes would have strengthened the ruling Morena party’s grip on power. So smaller parties that are Morena allies joined the opposition to strike the bill down.

On UMSCA, I’m encouraged that there seems to be understanding about some shared goals including stricter rules of origin and on transshipments was a way to strengthen regional supply-chain resilience5. The endgame may be three bilateral deals or a more open-ended type of USMCA, that I am less sure about. Also keep in mind the US has been more assertive in Latin America, so deliberately undermining its main trading partner seems contrary to this goal, particularly when the US’ priority seems to derisk supply chains from China6.

Figure 1: Eroding business confidence suggests investment weakness likely to persist (3mma, seasonally adjusted indices)

LA: Assuming an outcome for the USMCA talks that leaves regional integration intact, where are the opportunities?

FG: Mid-caps underperformed larger names since December, so their valuations look compelling. I see this relative de-rating as a function of shifts in foreign flows and not of worse fundamentals among mid-caps. Within this group, real estate is an interesting spot which has seen positive earnings revisions and is a play on further nearshoring through industrial land. Second, I think that materials’ companies are reflecting a lot of good news, even if global growth concerns linked to the war turn out to be short lived. So I see a case to rotate to domestic names like banks and staples. Last, I wouldn’t get too caught up in the discussion of whether Mexico grows 1% or 2% this year. The mid-cap space today offers opportunities in businesses with a track record of growing at a faster pace than the economy.

ABOUT TRG

Founded in 2002, The Rohatyn Group (TRG) is a global asset manager focused on emerging markets and real assets. Headquartered in New York the firm is comprised of ~100 professionals based in 14 countries across North and South America, Europe, the Middle East, Africa, India, Southeast Asia, and Oceania.

TRG investment capabilities span private and public asset classes focused on emerging markets as well of global forestry and agriculture investments. At the core of our business, we are dedicated to providing specialized investment solutions. Leveraging our global-meets-local approach, on-the-ground coverage, and extensive multidisciplinary investing experience we work strategically to address our clients’ unique needs.

Learn more at: https://www.rohatyngroup.com/

IMPORTANT INFORMATION – REFERENCES

1 Deutsche Bank. (2026, February 3). DB CoTD: An Oscar winning pack?

2 Peterson Institute for International Economics. (2026, February 24). Trump’s tariff revenue tracker.

3 Mexico Daily News. (2026, March 18). US and Mexico tout ‘historic’ security cooperation as DEA, Mexican officials meet in Washington.

4 Mexico Business News. (2026, February 4). Mexico launches MX$5.6 trillion investment plan 2026-2030.

5 Office of the United States Trade Representative. (2026, March 5). The United States and Mexico Launch Review Process of the USMCA.

6 BBC. (2026, February 4). US launches plan to tackle China’s critical minerals dominance.

IMPORTANT INFORMATION – DISCLAIMERS

The information provided herein is for educational and informational purposes only, and neither The Rohatyn Group nor any of its affiliates (together, “TRG”) is offering any product or service hereby. The information provided herein is not a recommendation, offer, or solicitation of an offer to buy or sell any security, commodity, or derivative, nor is it a recommendation to adopt any investment strategy or otherwise to be construed as investment advice. Any projections, market outlooks, investment outlooks or estimates included herein are forward-looking statements, are based upon certain assumptions, and should not be construed as an indication that certain circumstances or events will actually occur. Other circumstances or events that were not anticipated or considered may occur and may lead to materially different outcomes. The information provided herein should not be used as the basis for making any investment decision.

Unless otherwise noted, the views expressed in the content herein reflect those of the authors set forth and are not necessarily the views of TRG. In fact, the views of TRG (and other asset managers) may diverge significantly from certain of the views expressed in the content herein. The views expressed in the content herein are subject to change without notice, and TRG disclaims any responsibility to furnish updated information in the event of any such change in views. Certain information contained herein has been obtained from third-party sources. While TRG deems such sources to be reliable, TRG cannot and does not warrant the information to be accurate, complete or timely, and TRG disclaims any responsibility for any loss or damage arising from reliance upon such third-party information or any other content provided herein.

Exposure to emerging markets generally entails greater risks and higher volatility than exposure to well-developed markets, including significant legal, economic and political risks. The prices of emerging market exchange rates, securities and other assets are often highly volatile and movements in such prices are influenced by, among other things, interest rates, changing market supply and demand, external market forces (particularly in relation to major tradingpartners), trade, fiscal and monetary programs, policies of governments and international political and economic events and policies. All investments entail risks, including possible loss of principal. Past performance is not necessarily indicative of future performance.

The information provided herein is neither tax nor legal advice. You must consult with your own tax and legal advisors regarding your particular circumstance.